Private school isn’t cheap, but there are many strategies for families to enroll their kids in excellent institutions without breaking the bank. When you’re managing month-to-month finances, the cost of tuition and associated fees can feel overwhelming—but it’s worth investigating your options.

“Don’t be shy about asking about needs‑based scholarships and applying,” says Elena Holeton, director of admissions at St. Clement’s School in Toronto. “Admission offices want these conversations. Many families stretch to afford independent schools, and questions about financial aid are quite common.”

Making independent schools more inclusive is a win for everyone. “Diversity enriches campus life in countless ways,” says Graham Brown of Brookes Westshore School in Victoria, BC. “You bring in motivated students from all backgrounds. That benefits everyone in the classroom.”

If you believe independent education is the right path but aren’t sure you can afford it, don’t worry—there are many ways to make it work.

18 Tips to Afford Private School

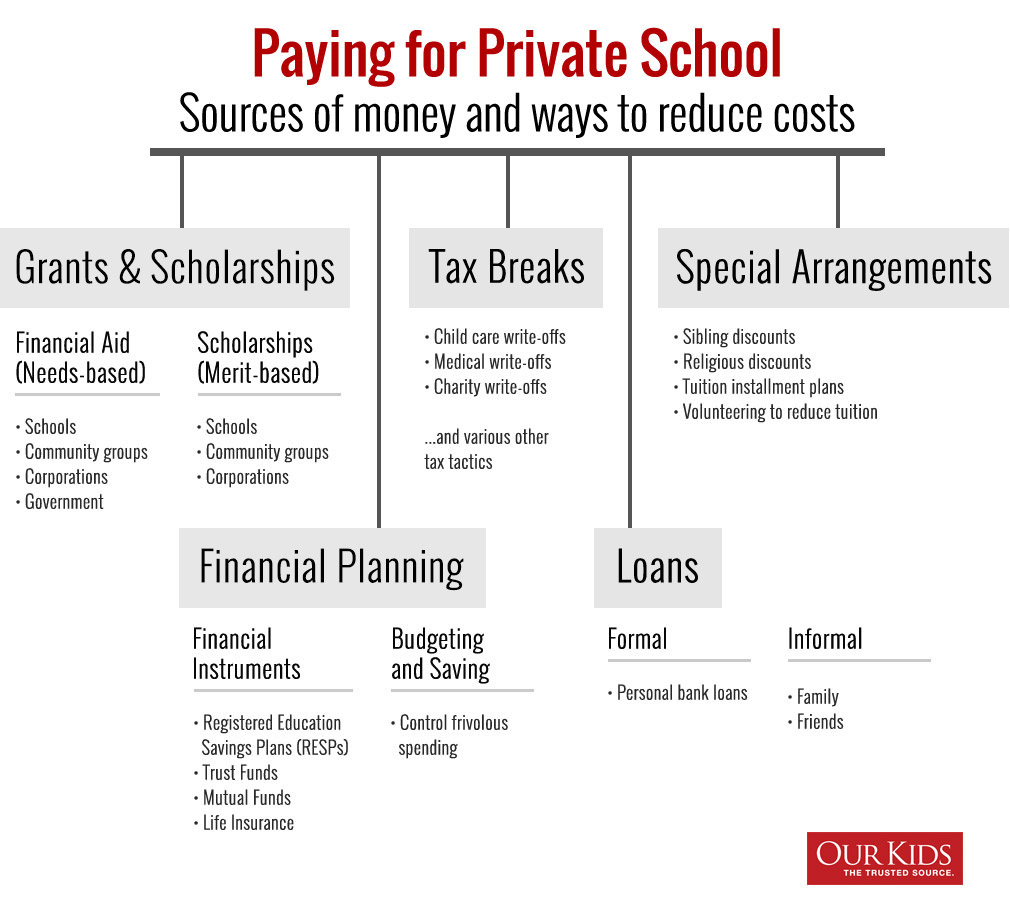

- Keep an open mind: Financial aid has increased in recent years. Schools are actively supporting more diverse families.

- Shop around: Tuition varies. Some schools offer affordable options, while others include services in the cost.

- Ask all your questions: Be open about finances. Schools may offer solutions, jobs, or flexible plans.

- Payment plans or volunteering: Many schools offer monthly plans; some accept volunteer work toward tuition.

- Multiple-child discounts: Particularly at faith-based schools, siblings often receive 10%+ discounts.

- Apply for financial aid: Most schools offer bursaries or scholarships—don’t assume you won’t qualify.

- Apply early: Aid is limited and available on a first-come, first-served basis. Start your application as early as possible.

- Community scholarships: Look for non-academic grants from clubs, churches, sports groups, and businesses.

- Be transparent: Provide accurate info when applying for aid. Be clear about special financial circumstances.

- Corporate scholarships: Some employers offer private school bursaries. Ask your HR department.

- Tax breaks: Religious tuition may qualify as a charitable donation. Special needs tuition may offer tax credits.

- Government support: Use programs like the Canada Child Benefit or CWELCC if eligible.

- Budget wisely: Cut back in some areas (e.g. vacations or cars) to afford school fees.

- Start saving early: Use a TFSA, RESP, or other savings tools to build a private school fund over time.

- Use life insurance: Whole-life policies can double as university savings accounts for your child.

- Ask grandparents: Many relatives want to support education and may contribute to tuition.

- Budget for extras: Plan for uniforms, transportation, and field trips. These add up quickly.

- Calculate built-in savings: Some private schools include meals, tutoring, or sports, which saves you money elsewhere.

Helpful Resources